11th April, 2021

🐘 Name

After #RedPeak a few years ago you'd think I would have learned my lesson about open letters, but apparently not. Let's try another one...

Dear Mark,

I write as a fan.

I'm worried that you're in the process of selling the prime headlands to folks who only just got here for an amount that, in generations to come, will feel pretty insignificant.

The media reports I've read have focussed on the lump sum amounts - $465m of new investment - and less what it will cost - a percentage of all future commercial revenues.

However, the most concerning part for me is not the dollars, or who gets them. It's the emphasis on the expertise that the new investors apparently bring. We appear to be conceding “we can't do this ourselves, we need help from overseas”.

We would never do that with the “teams in black”. Hiring successful players and coaches from overseas, late in their careers, and hoping they will somehow magically make them better is something that Australia or England or Wales or Ireland do. We always prefer to develop our own talent1.

So why is this different?

And, for context, every venture fund and private equity investor talks up the skills and expertise they have, and how much they can help, in addition to just writing a big cheque. But, with the benefit of hindsight, very few actually end up contributing more value than they capture.

Here is the problem with this kind of deal, from my perspective: NZR is a forever owner. There is no scenario where we ever want to “exit”. But that's not true of the new investors you are talking to. They all have funds with a limited lifetime and investors of their own who will eventually want a return. One day they will want to sell their shares to somebody else. Then what?

So, there is a mismatch.

It's also interesting that when I talk about the organisation you lead I say “we” and not “you”. I'm part of a very large group who feel a sense of ownership, even if it's not financial (“stakeholders” is the fancy word that people use these days, right?) I guess, in the spreadsheets, we are the ones who will eventually be repaying that $465m amount, with interest, by purchasing television subscriptions, branded jerseys, tickets to the games, etc.

Which does make me wonder if there is a way to do this without creating that mismatch.

If I understand it the proposal is that $50m will be invested in the new commercial entity, and about the same amount again will be distributed to provincial unions. Those are big numbers, but not relative to the huge amount of cheap capital in the world right now. You'd probably even get a decent chunk of that from the same big group of stakeholders I mentioned above if you asked us. And all without having to sell any part of the golden goose.

Of course, it would mean putting heads down and doing the hard work to actually build the commercial team directly and develop those assets and revenue streams to pay for that. It's not going to be easy. But, putting promises from private equity folks aside, you're going to have to do that either way. And, anyway, isn't building world class teams from local talent what has made NZR famous in the first place?

I wish you luck.

A fan xx

🏒 Grow

Two weeks ago I wrote about the different ways that teams report their results - some focus on size ("Net profit was $15m"), some on growth ("Revenue increased 9%") and others still on acceleration ("We added 100k new customers in the last year, 70k in the last quarter"). I suggested that paying attention to which is used where gives us insight to what the organisation is focussed on.

Now, let's narrow in on the special case where all three are positive - i.e. good numbers, growing fast and accelerating over time. Often, incorrectly, start-ups will refer to this as exponential growth, or “hockey stick” growth.

(This makes much more sense once you realise that this expression is imported from North America where “hockey” means “ice hockey” not “field hockey” - the sticks are a different shape!)

Unfortunately I've seen that terminology mislead a number of people who are working on new things over the years. They hear it and mistakenly think that growth is either a hockey stick or a pool cue, and that you can't tell one from the other until the last moment. So they flail away, with numbers that are not growing let alone accelerating, and hope that the inevitable up-tick is just around the corner.

But, when you look closer at those things that have grown to become large, that is not typically what happens at all.

Some examples...

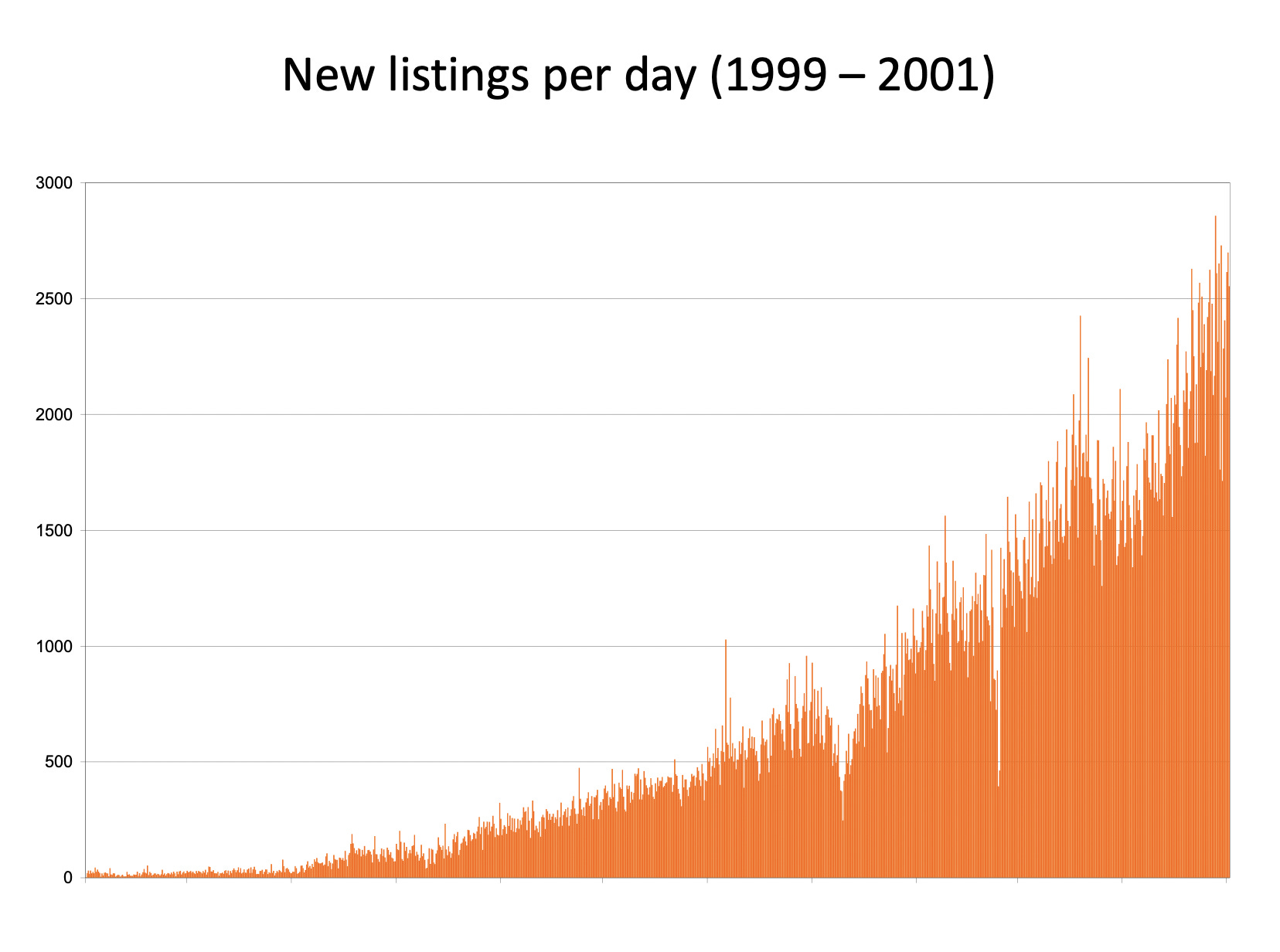

In 2006 I was privileged to speak about Trade Me at the very first Webstock in Wellington2. I showed two graphs to demonstrate the growth in new listings on the site:

The first showed the results from the first two years of operations. You can see it took a few months to get going then the number of listings accelerated from there, giving the graph a familiar “up and to the right” shape.

The second graph showed the full period of time up until the point I was speaking (so ~7 years worth of data). The blue box outlines the area that was shown in the first graph. You can see that the growth that followed had made that period look very flat by comparison.

(Btw, the big dips each year are Christmas)

My access to that data set ended a couple of years after that, but it would be fascinating to see the shape of this continued over the years since then. As Tim O'Reilly has noted, what people assume to be exponential growth is nearly always sigmoidal, given enough time. But that's a story for another day, for now let's focus on the take-off phase rather than the cruise and landing.

The important thing to note is that the shape of these graphs is remarkably similar. The numbers in the first graph are much smaller, and when you look at that same time period retrospectively it looks flat, but when you zoom in, or more importantly when you are living in that moment it's not flat at all.

Trade Me grew from 10,000 members when I first started to around 100,000 in the first year I worked there and kept growing. The key numbers - listings, completed listings, unique visitors, unique sellers, etc - were all growing through that time period, even though we look back later and think that the actual numbers then were small.

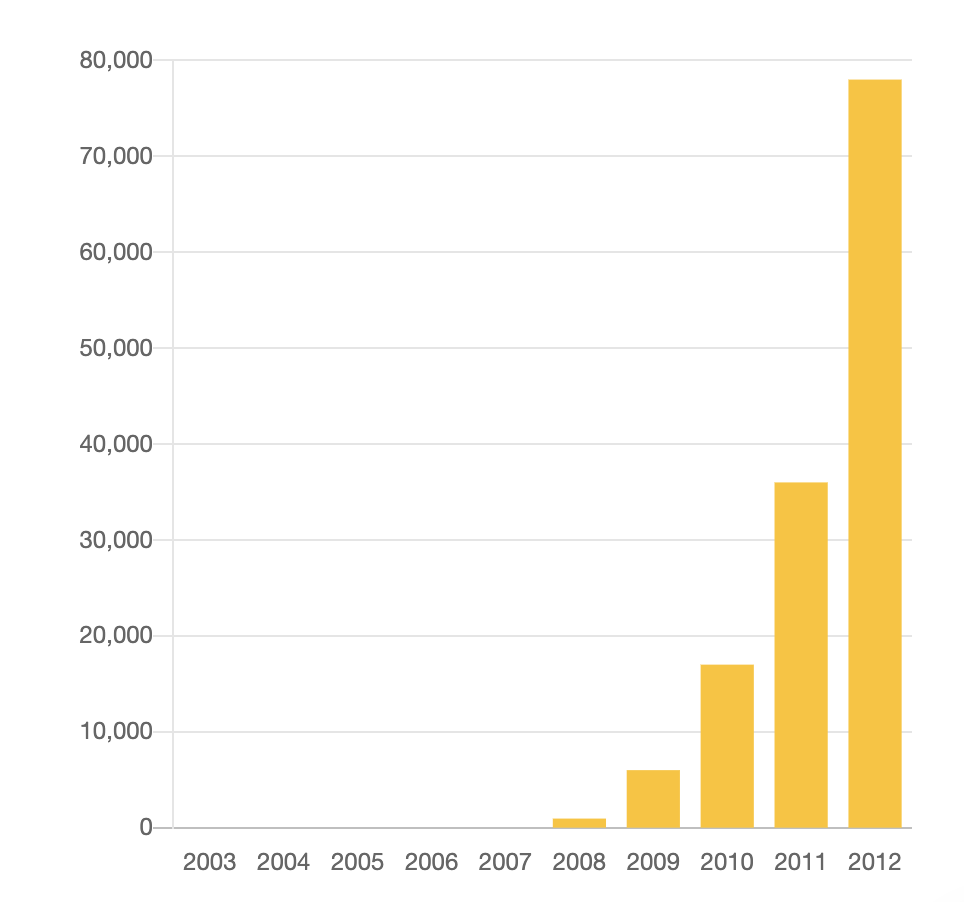

Likewise, consider the growth in Xero's subscriber base...

When we plot this over different time periods we see a very similar pattern3:

The growth in the first five years looks amazing - from 950 subscribers in 2008 to 78,000 in 2012.

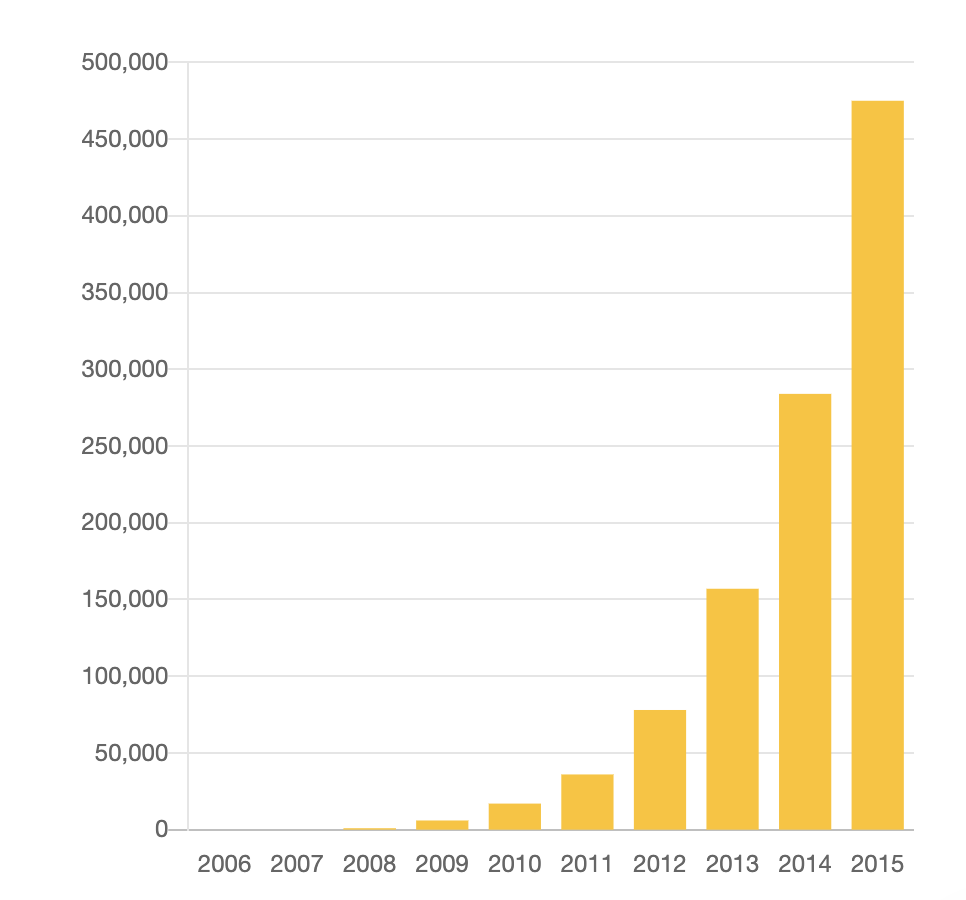

When we expand that to include the first eight years, those first five years suddenly look much less impressive. By then they had reached 475,000 subscribers.

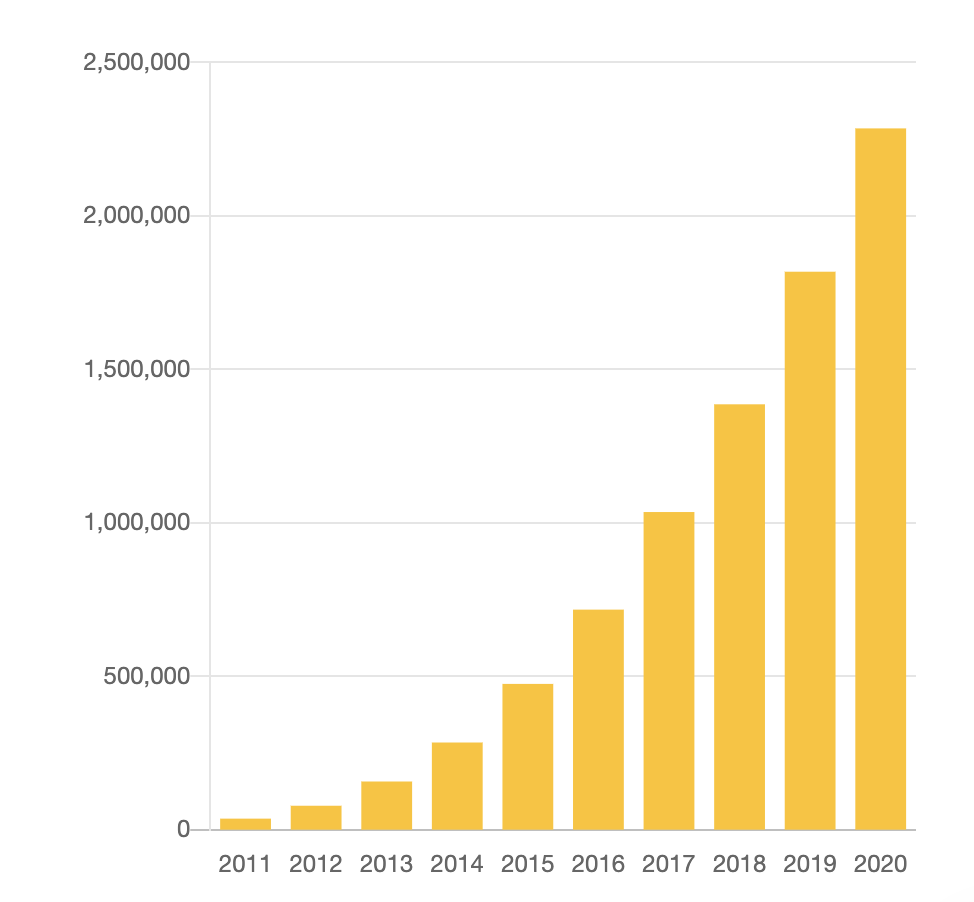

And when we consider in the context of the FY20 results … by now those early years are nearly rounding errors.

Again, the numbers in the beginning are small, so looks flat in retrospect, but are actually significant in real-time - e.g. growing from 950 to 6000 subscribers in the second year, and then nearly tripling again the following year to 17,000.

And, as with the Trade Me results, the shape of the growth is pretty consistent, no matter what time period you are looking at.

“Intensity makes a good story but consistency makes progress”

— James Clear

So, what's the lesson here?

Firstly, if you're working on something that needs to grow in order to be successful then it's really important to have some measure that is actually growing right away. I'm not sure that it even matters what that thing is, especially at the very beginning. But if all of your numbers are flat then you're likely not on a growth path.

Secondly, you need to balance patience with milestones along the way. As we've seen, even the companies that eventually achieve remarkable growth4, all start off with relatively modest actual numbers. But they constantly grow, and compound that growth. So, while it's great to dream big, it's necessary to break those ambitions down into smaller more digestible chunks, so you can understand where you need to be next year, next month and next week in order to still be on track to where you want to be at the end (however you define “the end”).

If you get this right then you can eventually join the group of founders who get to look back and sarcastically describe your venture as an overnight success.

🛂 Import

Let me make more-or-less the same point twice in one post...

It's ironic, and frustrating, that whenever we turn our mind to innovation or technology or start-ups or investment or even branding our first instinct seems to be “what solution can we import from overseas?”

We seem very attracted to the idea of being second (a la Hollywood vs Wellywood).

But, what are we the first of?

🇺🇸 Silicon Valley

One of the ideas we seem to love, almost as much as being world class and punching above our weight, is the idea that we could be the next Silicon Valley.

For example, speaking to the recent McGuinness Institute “Mission Aotearoa” event, NASA Chief Scientist Dennis Bushnell proposed that NZ should become “the preferred place to live and operate from for folks that ideate [Ed: 🙄], invent and create the future” and noted that “his friends all over the world wanted to move here”.

Wonderful!

Reading between the lines, in case it's not obvious, he's saying that those type of people come from somewhere else, not here, and the obvious solution is taking all the Silicon Valley imports we can get (who presumably can't wait to get out of where they are right now).

This is really misguided, in my opinion. We don't need an influx of rich old folks, towards the end of their careers, to come here to retire. That won't help us as much as some imagine. It's well established now that investors are happy to put capital into businesses started here without us having to attach a residency permit to that money5 (although, of course, they want to have the option to live here, so if that is offered expect them to take it without question!) The price we put on our passports should be much higher. And, anyway, when we have tried this specifically in the past there hasn't been a high retention rate!

It also massively overlooks the factors that led to the creation of the first Silicon Valley.

If you're reeeeeally interested in this stuff then I throughly recommend you watch this dense talk by Steve Blank (this is definitely one you can watch at 1.5x):

Secret History of Silicon Valley (not so secret when you post it on YouTube eh Steve!)

The tl;dr is: the formula to create a Silicon Valley is simple 🤨, all you need is an established world class university, a cold war and the corresponding massive increase in military funded R&D projects, ex-military professors and managers with radically different views on the link between academic research and private business, a government willing to be a significant customer of the new businesses created by this via large defence contracts, and a bunch of wealthy families prepared to take risks on funding the various private companies that are created (incentivised by cuts in capital gains tax rates and changes to pension fund rules).

Easy!

Let's not pretend that we can re-create any one of those inputs in New Zealand at short notice, let alone all of them.

And, even if we could ... then we'd be Silicon Valley.

What I think people pushing this idea really want is all of the good bits of Silicon Valley but without all of the bad bits. This is a little like hoping that your kids will inherit all of your favourable traits but none of your vices.

To pick one example: You sometimes hear people saying we need to embrace failure like Americans do. You rarely hear those same people say we need to tolerate success like Americans do. But they are two sides of the same coin. Viva la inequality, eh!

So, when you say that New Zealand could be the next Silicon Valley I assume either (a) you don't really understand Silicon Valley; and/or (b) you don't really understand New Zealand.

🇮🇱 Israel

Another country that we are encouraged to emulate is Israel. Perhaps because they are about the same size as us and have been very successful.

In the early 2000s we enthusiastically copied their program to bootstrap a local venture capital sector, with remarkably poor results. We called ours the New Zealand Venture Investment Fund, and I'll write a whole separate thing about this next week. But in the meantime, let's just note that the pattern here is frustratingly familiar.

What we wanted was their outcomes. And we copied their strategy. We seemingly didn't pay any attention to their context, or the unique factors that enabled their success, that we were never going to re-create (what a business considering a strategy might call “competitive advantages”).

Specifically in the case of Israel, their compulsory military service and the massive immigration they experienced immediately prior to their boom.

When I visited Israel a few years ago one of the biggest lessons what this: the first question potential investors ask founders is “What unit did you serve in?” This is a simple filter to quickly understand more about the sort of training and networks the founders were exposed to during their two years in the military. When the answer is “Unit 8200” then the next question is quickly “How much can I invest!” Of course, in New Zealand, we have nothing that even approximates that.

Then you discover how many of the senior people you meet working in their ecosystem, as investors, mentors and/or advisors, are folks who moved to Israel from former Soviet states in the late 1980s. There was a 25% population increase in 10 years, and a large number of those people were qualified scientists, engineers and mathematicians who played pivotal roles in many of the early successful ventures and venture funds6.

Throw into the mix a lack of natural resources and a constant existential crisis (another repeating pattern) and you have a good mix of ingredients that we in New Zealand will never have (fingers crossed!)

And then we wonder why it didn't work!

🇫🇮 Nokia

A third and final example:

Older readers may nostalgically recall when what we really really wanted in New Zealand was our own Nokia, so we could be a bit more like Finland.

Nokia was an old company that transformed itself from a pulp and paper producer into a hugely successful electronics companies in the 1990s. At one point Nokia accounted for 25% of all R&D spend in Finland and nearly 3% of GDP. More remarkably in 2000 they represented almost 33% of total GDP growth for the whole country. We loved the idea of turning a primary producer into an innovation powerhouse for the whole country.

Curiously, you don't hear that specific goal referenced so much any more, post iPhone. In 2013 Nokia sold its phone division along with a giant pile of patents to Microsoft for €5.4 billion.

Even in Finland they have changed their strategy. Business Finland’s CEO Pekka Soini recently said:

“Finland shouldn’t rely on ‘one national champion’ like Nokia again, but should push smaller companies to increase their R&D spending and to adopt new technologies”.

Just mindlessly copying others’ solutions has not worked for us and is not going to work. Our context is different. Our values are different. We need to think much better about the future than that.

The questions we should be asking instead are: What are our strengths and how can we leverage those to create success for ourselves? And, what are our constraints and how can we reduce or remove them?

Paul Callaghan's mantra, in response to this question was:

“Be the place where talent wants to live”.

There are, of course, multiple ways to read this:

Are we the place where talented New Zealanders, born and educated here, want to stay?

Or, are we the place where talented people from around the world want to come and work - that could be to study, or complete research, or start a business, or work on an existing business?

Of course, both! But the tactics required for each are very different.

We're not going to convince anybody to stay by turning ourselves into a second-rate derivative version of what they can easily get directly overseas.

And, those we need to attract are more usefully qualified immigrants, hungry for future success, than billionaires wanting a comfortable retirement playground. A much more interesting question is: why don’t we currently welcome more of them?

Top Three is a weekly collection of things I notice in 2021. I’m writing it for myself, and will include a lot of half-formed work-in-progress, but please feel free to follow along and share it if it’s interesting to you.

I acknowledge there are many in the Pacific Islands who might read that sentence and frown.

Unfortunately this seems to be the forgotten Webstock - you won't find much reference to it on their web site, or any recordings of the talks - but it was a wonderful experience for me and one of the very first opportunities I had to speak in public about the things we'd been working on at Trade Me - all these years later I’m still grateful to Tash and Mike for that moment.

These graphs come from this One Metric data set: https://app.onemetric.io/r/tRjY41tfYQBBzDeXUABYu49R

Pre-Covid this got to the ridiculous situation where government agencies were paying for successful investors to visit to sprinkle some of their magic dust on us. In my opinion, when cashed-up folks from overseas are so excited about visiting that we need to pay for their flights then we’ve likely misunderstood their enthusiasm. Hopefully that’s one thing we can consign to history when borders are reopened

Interesting to note, in the most recent stats I could find, from 2019, Israel reference the country of origin (73.8% from former USSR states) and education levels of immigrants (74.8% of them had 13 or more years of schooling), but don’t mention wealth at all.